Chapter – 1 Introduction of an Economy (Micro Economics)

Chapter – 1.

Introduction

of an econnomy

1.1

A Simple Economy and the Central Problems of an

Economy

1) Q:

What do you mean by Economics?

Economics is the study of how

individuals, households, and society choose to allocate their highly scarce

resources to satisfy their unlimited human wants .

Root

Cause: The

absolute root cause of all economic issues is scarcity. (V.V.V imp)

2)

Q: What do you mean by scarcity: (imp)

It is defined as excess of demand over available

supply, i.e., demand of resources greater than supply of resources.

3) Q: What do you mean by

a Simple Economy?

A simple

economy is an introductory model of a society where independent individuals

act as both producers and consumers to fulfil their needs through mutual

exchange.(like a farmer growing corn) and trade away their surplus to get other

daily necessities .

4)

Q: Why does the “Problem of Choice” arise in

every economy?

Every

economy have limited resources and resources have their alternative uses. the problem

of choice arises due to scarcity of resources .

5)

Q: What are the fundamental economic problems being

faced by any society?

completely

unlimited human wants and highly scarce resources .

6) Q:

What specific bundle of resources does a family farm, a weaver, a school

teacher, and a poor labourer own in a society or in a simple economy?

1.

Farm: Agricultural Land Plot, Seed

and Grain Stocks, Cultivation Equipment, Animal, Human Labour

2.

Weaver: yarn and cotton, Machinery for weaving cloth.

3.

Teacher: Specialized mental skills

and knowledge.

4.

Labourer: no resource excepting

their own labour services.

7) Q:

What is the exact formal definition of ‘goods’ in economic terms, and what are

its examples?

1.

Tangible Goods are physical, material

objects that a person can see, hold, and touch .and used specifically to

satisfy the various material wants and needs of individuals. Ex: Fan, computer

2.

Intangible Character: Services are

non-physical actions or tasks that cannot be touched. Services are created to fulfil

human desires and provide utility through action. Ex: service of teacher,

doctor

8) Q:

What does the term ‘individual’ actually mean as a decision-making unit in

economic text?

Individual does not merely signify a

single separate human being; it means any single cohesive decision-making

entity in the economy. ex: Single Humans, Collective Households (family), Organisations:

.

9) Q:

Why must there be compatibility between collective production and collective

consumption in an economy?

Total

production choices made by all units together must match up perfectly with the

total consumption desires of the whole population because we assume the society is completely

isolated, meaning all items consumed must be grown or made internally with zero

outside imports .

10)

Q: What happens to resource allocation if

society collectively produces more corn or less corn than what people actually

want to consume?

- Overproduction

Adjustment:

resources must be moved out of farming to produce other goods that are in

high demand by the public .

- Underproduction

Adjustment:

the economy must step in and change its resource map. Society must take

inputs away from other goods and reallocate them into growing more corn to

satisfy the public.

11)

Q: What are the three specific central problems

that every single economy must solve? (imp)

- What to Produce: Deciding exactly which

goods and services are to be produced and in what total quantities.

- How to Produce: Deciding the exact

methods, resource combinations, and techniques used to create those chosen

goods

- For Whom to Produce: Deciding the final

distribution layout to determine who gets how much of the finished

national output

12)

Q: What detailed choices and trade-offs come

under the central problem of ‘What to produce and in what quantities’?

Food Vs Luxury Dilemma: A society must choose

whether to allocate its scarce land and factories to produce basic food,

clothes, and housing, or high-end luxury items

13)

Q: What detailed choices regarding resource

combinations and techniques come under the central problem of ‘How to produce’?

Producers

must choose whether to adopt a technique that uses more human hands

(labour-intensive) or one that relies heavily on mechanical equipment

(capital-intensive)

14)

Q: What detailed choices regarding the final

share of distribution and minimum standards come under the central problem of

‘For whom to produce’?

|

Test 1.1 1.

Among the competing usage of resources, the main cause of the

“Problem of Choice” in economy (MP 2026) (A) Abundance of resources (B)

Scarcity of resources (C) Misuses

of resources (D)

No uses of resources 2.

The fundamental economic problems being faced: (MP 2025) (a) Unlimited human

wants (b)

Limited wants and unlimited resources (c) Unlimited wants and scarcity resources (d) Limited wants and limited resources 3.

What do you understand by the term “Scarcity”? Explain how

scarcity acts as the root cause behind the problem of choice and list the

three central problems that every economy must solve.

|

1.2

Production Possibility Frontier and Opportunity

Cost

15)

Q: What do you understand by the production

possibilities or the Production Possibility Set of an economy?

A Production

Possibility Set is the complete collection of all the different

combinations of goods and services that an economy can possibly produce using

its given resources and available technology

16)

Q: What are the fixed parameters or conditions

assumed when determining the Production Possibility Set of an economy? Or

assumption of ppc curve (imp)

Assumptions of the

Production Possibility Frontier (PPF)

- Fixed Quantity of

Resources:

The total stock of productive resources available in the economy is

completely fixed and given.

- Constant Technology: The state of

technology and technical knowledge remains unchanged throughout the

analysis.

- Full and Efficient Employment: All available

resources are assumed to be fully utilized and employed with maximum

efficiency (zero wastage).

- Transferable Resources: Resources are not

specific to one job; they can be freely shifted from the production of one

good to another.

- Two-Good Economy Model: For simple graphic

representation, it is assumed that the economy produces only two distinct

goods (e.g., corn and cotton).

17)

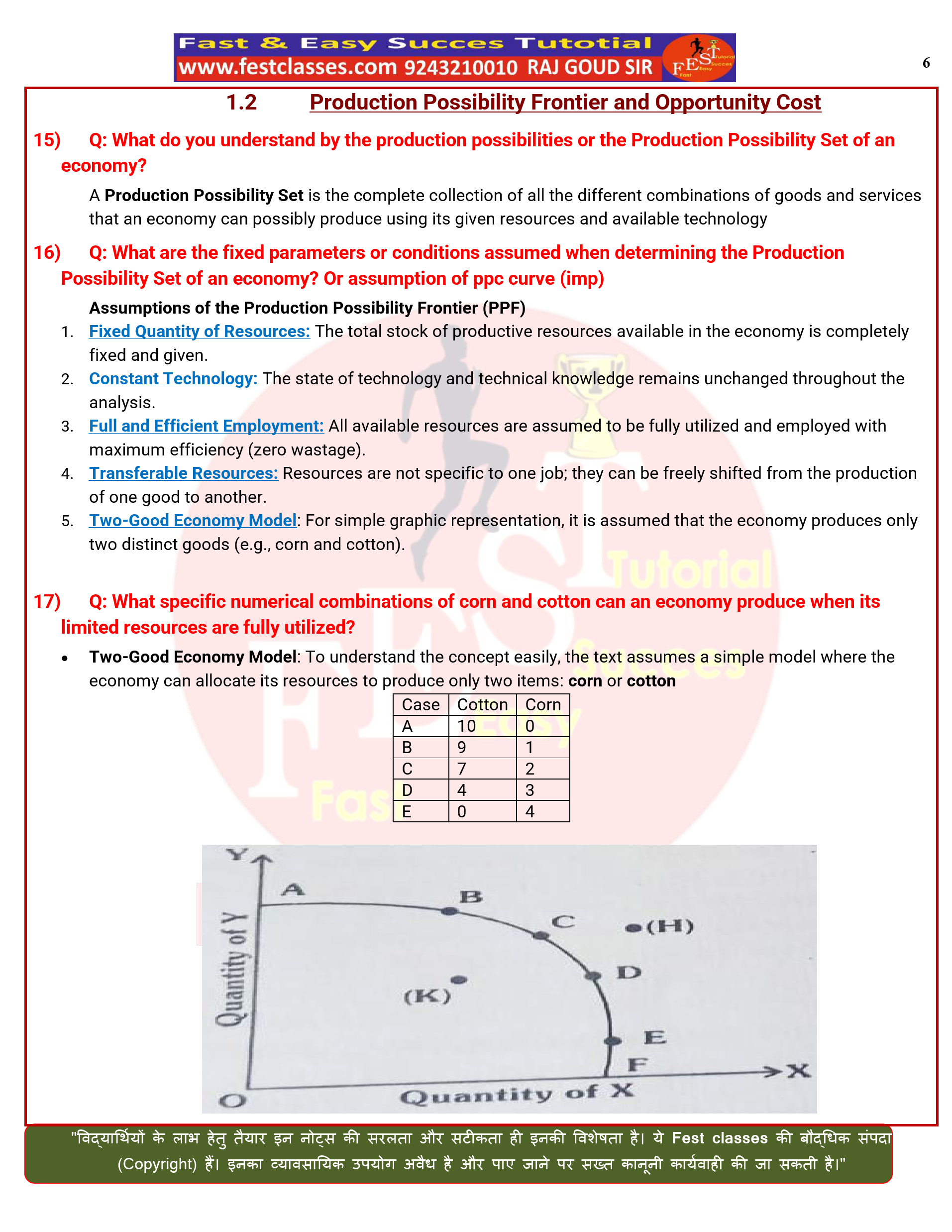

Q: What specific numerical combinations of corn

and cotton can an economy produce when its limited resources are fully

utilized?

- Two-Good Economy Model: To understand the concept easily, the text

assumes a simple model where the economy can allocate its resources to

produce only two items: corn or cotton

|

Case |

Cotton |

Corn |

|

A |

10 |

0 |

|

B |

9 |

1 |

|

C |

7 |

2 |

|

D |

4 |

3 |

|

E |

0 |

4 |

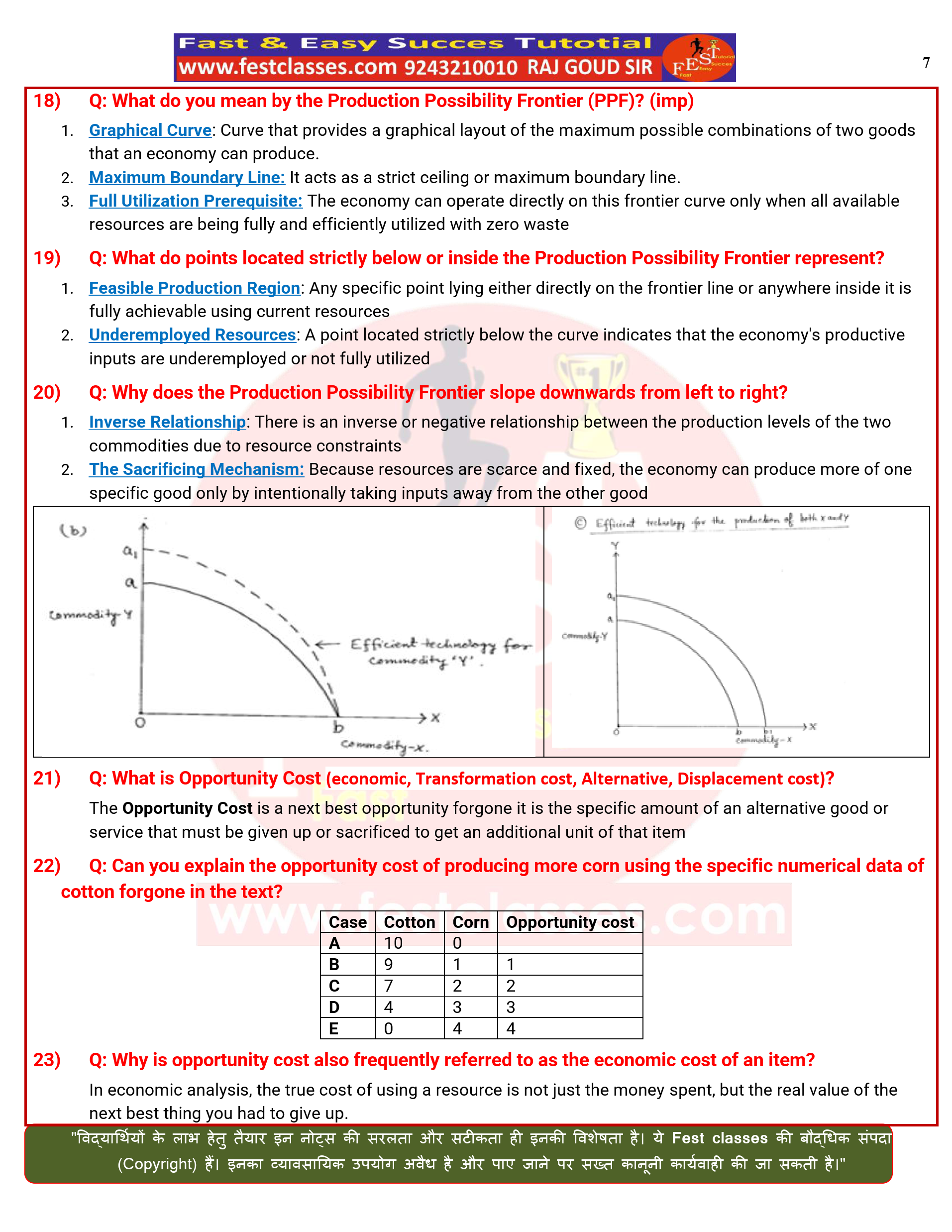

21)

Q: What do you mean by the Production

Possibility Frontier (PPF)? (imp)

- Graphical Curve: Curve that provides a

graphical layout of the maximum possible combinations of two goods that an

economy can produce.

- Maximum Boundary Line: It acts as a strict

ceiling or maximum boundary line.

- Full Utilization

Prerequisite: The economy can operate directly on this frontier curve only when

all available resources are being fully and efficiently utilized with zero

waste

22)

Q: What do points located strictly below or

inside the Production Possibility Frontier represent?

- Feasible Production

Region:

Any specific point lying either directly on the frontier line or anywhere

inside it is fully achievable using current resources

- Underemployed Resources: A point located

strictly below the curve indicates that the economy’s productive inputs

are underemployed or not fully utilized

23)

Q: Why does the Production Possibility Frontier

slope downwards from left to right?

- Inverse Relationship: There is an inverse

or negative relationship between the production levels of the two

commodities due to resource constraints

- The Sacrificing

Mechanism:

Because resources are scarce and fixed, the economy can produce more of

one specific good only by intentionally taking inputs away from the other

good

|

|

|

26)

Q: What is Opportunity Cost (economic, Transformation cost, Alternative, Displacement cost)?

The

Opportunity Cost is a next best opportunity forgone it is the specific

amount of an alternative good or service that must be given up or sacrificed to

get an additional unit of that item

27)

Q: Can you explain the opportunity cost of

producing more corn using the specific numerical data of cotton forgone in the

text?

|

Case |

Cotton |

Corn |

Opportunity cost |

|

A |

10 |

0 |

|

|

B |

9 |

1 |

1 |

|

C |

7 |

2 |

2 |

|

D |

4 |

3 |

3 |

|

E |

0 |

4 |

4 |

32)

Q: Why

is opportunity cost also frequently referred to as the economic cost of an

item?

In economic analysis, the true cost of using a

resource is not just the money spent, but the real value of the next best thing

you had to give up.

|

Test 1.2 1.

A collection of all possible combinations of goods and services that

can be produced in an economy with given resources and technology is

called: (MP 2024) (A)

Consumption Possibility Frontier (B)

Production Possibility Set (C) Market

Exchange Interaction (D)

Normative Allocation Frontier 2.

The amount of another good that must be sacrificed or forgone to

obtain an additional unit of a desired good is called ____________. (MP

2026) 3.

What is meant by a Production Possibility Frontier? Explain why it

slopes downwards from left to right using the concepts of resource scarcity

and opportunity cost. |

1.3

Organisation of Economic Activities

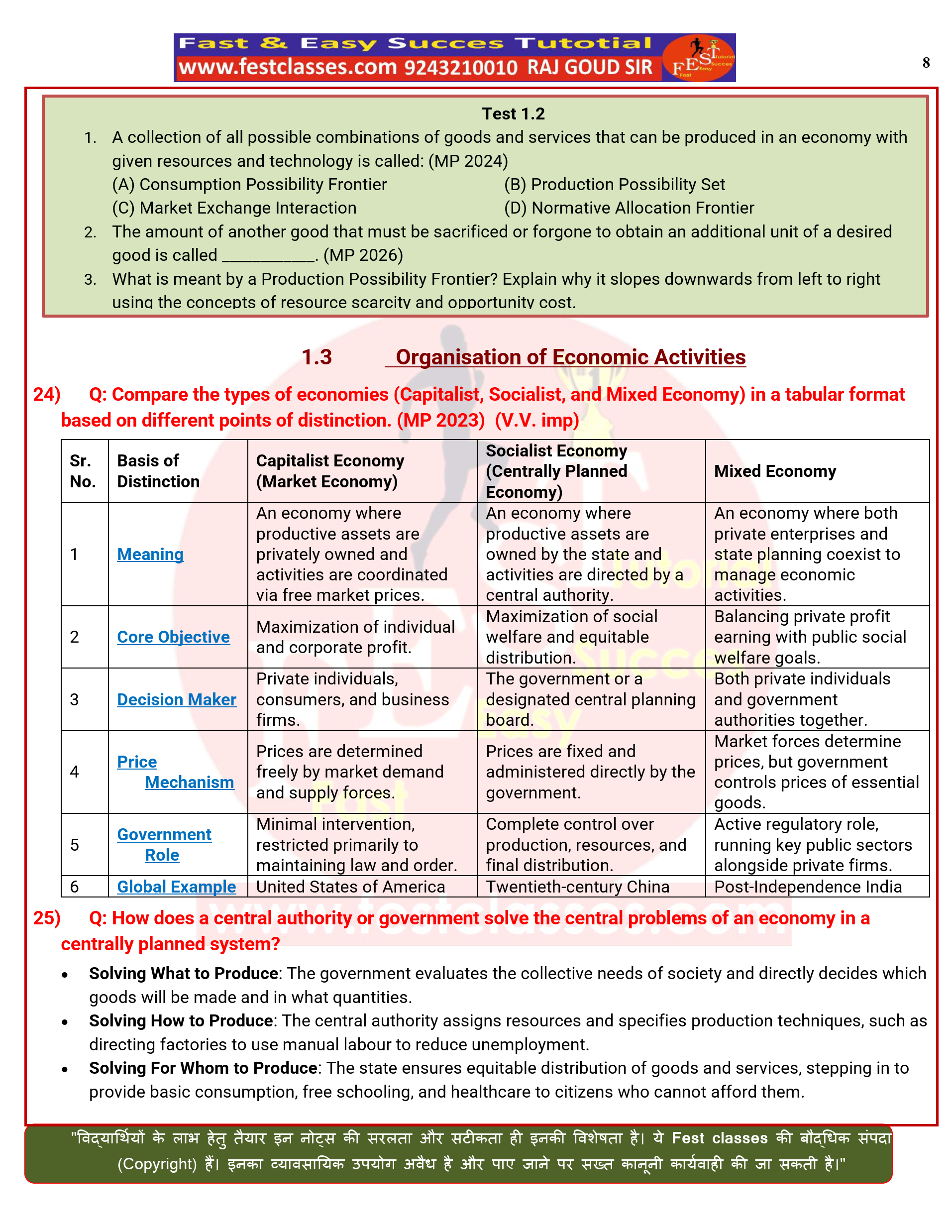

33)

Q: Compare the types of economies (Capitalist,

Socialist, and Mixed Economy) in a tabular format based on different points of

distinction. (MP 2023) (V.V. imp)

|

Sr. No. |

Basis of Distinction |

Capitalist Economy (Market Economy) |

Socialist Economy (Centrally Planned

Economy) |

Mixed Economy |

|

1 |

Meaning |

An economy where productive assets are

privately owned and activities are coordinated via free market prices. |

An economy where productive assets are

owned by the state and activities are directed by a central authority. |

An economy where both private

enterprises and state planning coexist to manage economic activities. |

|

2 |

Core

Objective |

Maximization of individual and

corporate profit. |

Maximization of social welfare and

equitable distribution. |

Balancing private profit earning with public

social welfare goals. |

|

3 |

Decision

Maker |

Private individuals, consumers, and

business firms. |

The government or a designated central

planning board. |

Both private individuals and government

authorities together. |

|

4 |

Price

Mechanism |

Prices are determined freely by market

demand and supply forces. |

Prices are fixed and administered

directly by the government. |

Market forces determine prices, but

government controls prices of essential goods. |

|

5 |

Government

Role |

Minimal intervention, restricted

primarily to maintaining law and order. |

Complete control over production,

resources, and final distribution. |

Active regulatory role, running key

public sectors alongside private firms. |

|

6 |

Global

Example |

United States of America |

Twentieth-century China |

Post-Independence India |

39)

Q: How does a central authority or government

solve the central problems of an economy in a centrally planned system?

- Solving What to Produce: The government evaluates the collective needs

of society and directly decides which goods will be made and in what

quantities.

- Solving How to Produce: The central authority assigns resources and

specifies production techniques, such as directing factories to use manual

labour to reduce unemployment.

- Solving For Whom to Produce: The state ensures equitable distribution

of goods and services, stepping in to provide basic consumption, free

schooling, and healthcare to citizens who cannot afford them.

40)

Q: What is the formal definition of a Market in

economics, and how does it differ from a common marketplace?

A market is a place where buyers and sellers can easily

contact each other to trade goods or services. Example: Buying a book from an

online website like Amazon or a local shop

41)

Q: How do price signals bring coordination and

solve the central problems of an economy in a market system?

- Reflecting Social

Valuation:

The mutually agreed price of a good represents how much society values

that item relative to other commodities.

- Coordination of Output: If buyers demand more

of an item, its price rises, sending a clear signal to producers to

reallocate resources and increase the production of that specific good.

- Factor Mix Allocation: Producers choose

resource combinations based on input prices, naturally selecting cheaper,

efficient technologies to maximize their profits.

Test 1.3

1. An economy in which all major economic decisions regarding production, exchange, and consumption are dictated by a central state authority is called a: (MP 2024)

(A) Capitalist Economy (B) Centrally Planned Economy

(C) Free Market Economy (D) Price-Signal Economy

2. An economy where some important decisions are taken by the government but economic activities are by and large conducted through the market is called a ____________ economy.

3. Write two distinctions between a Centrally Planned Economy and a Market Economy. (MP 2023)

1.4

Positive and Normative Economics, and Branches

of Economics

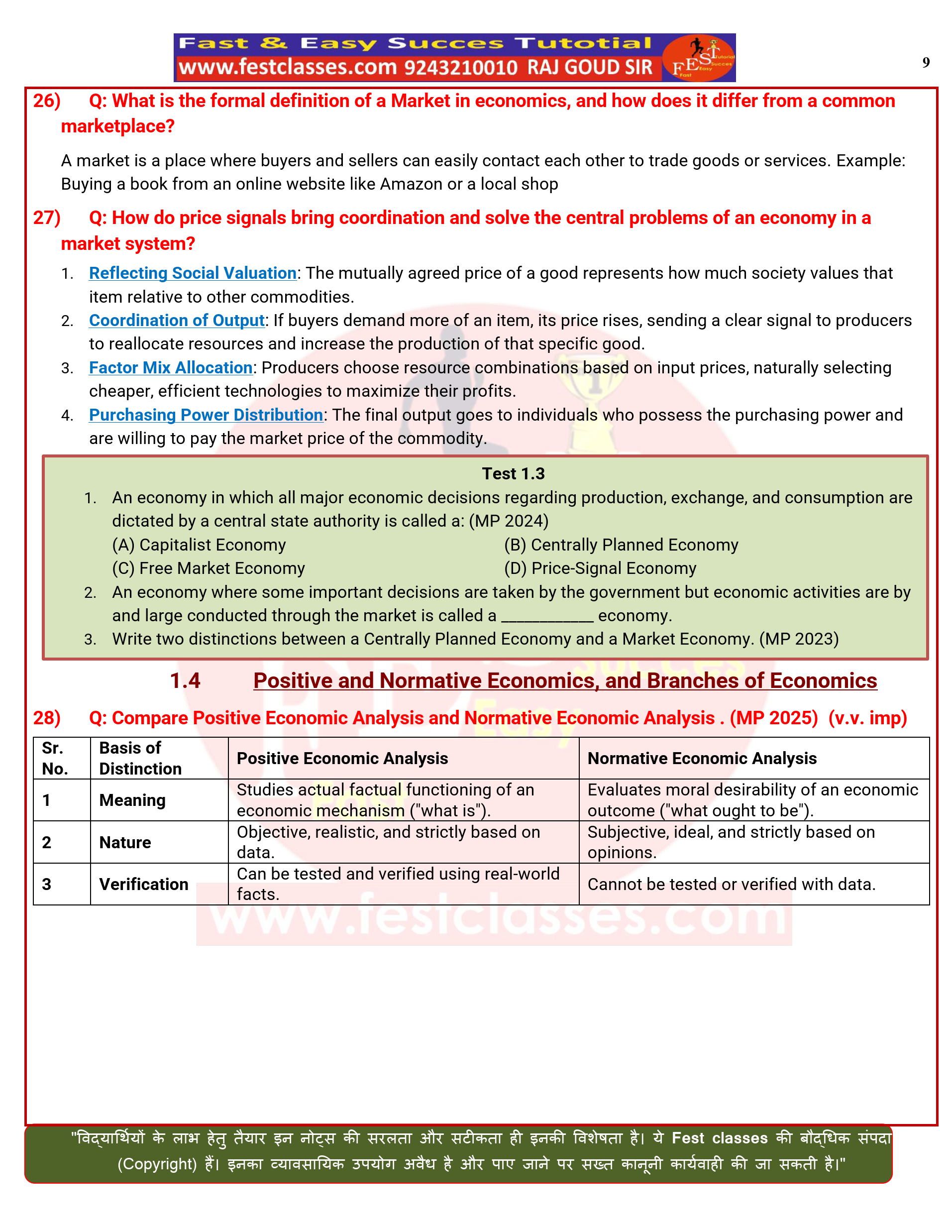

42)

Q: Compare Positive Economic Analysis and

Normative Economic Analysis . (MP 2025)

(v.v. imp)

|

Sr. No. |

Basis of Distinction |

Positive Economic Analysis |

Normative Economic

Analysis |

|

1 |

Meaning |

Studies actual factual

functioning of an economic mechanism (“what is”). |

Evaluates moral

desirability of an economic outcome (“what ought to be”). |

|

2 |

Nature |

Objective, realistic, and

strictly based on data. |

Subjective, ideal, and

strictly based on opinions. |

|

3 |

Verification |

Can be tested and verified

using real-world facts. |

Cannot be tested or

verified with data. |

47)

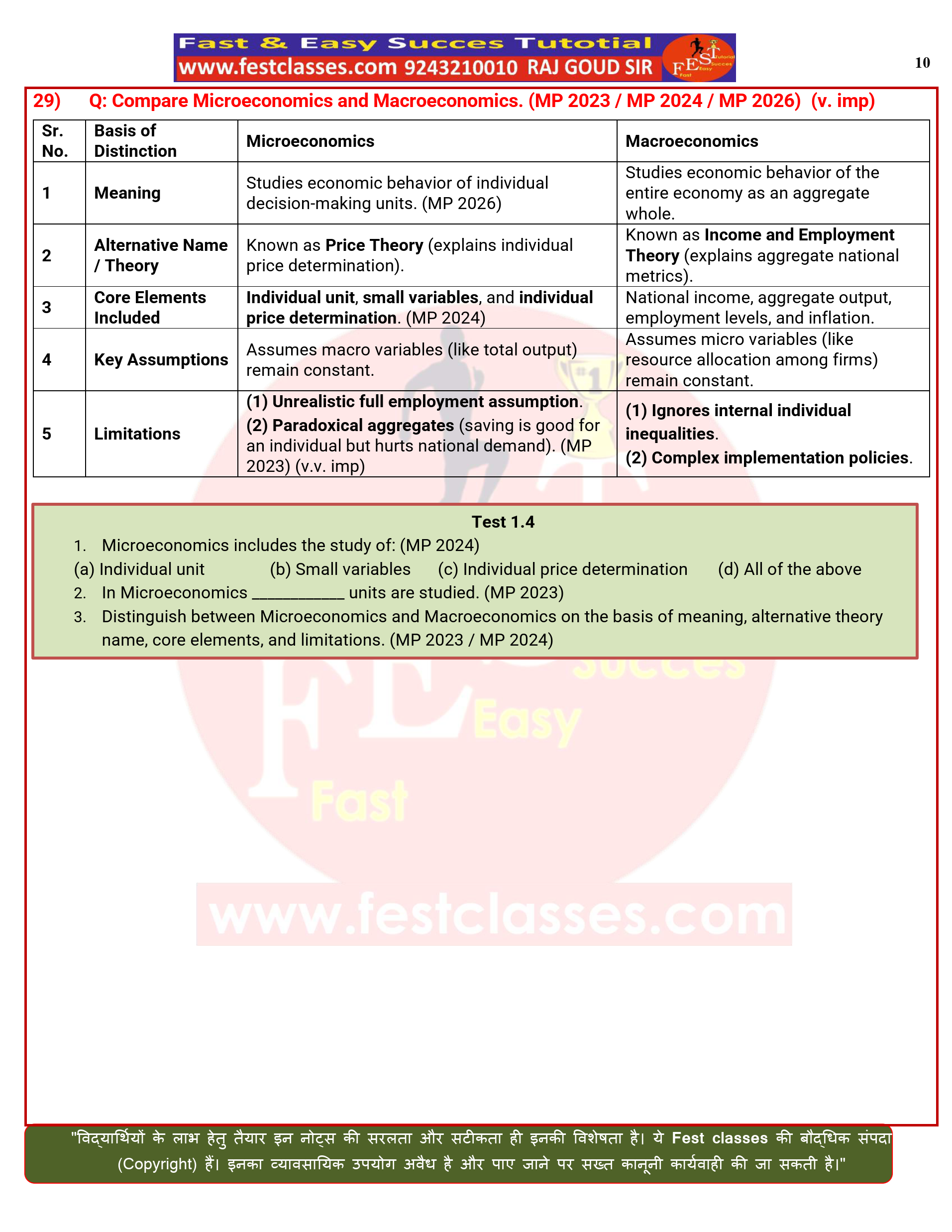

Q: Compare Microeconomics and Macroeconomics.

(MP 2023 / MP 2024 / MP 2026) (v. imp)

|

Sr. No. |

Basis of Distinction |

Microeconomics |

Macroeconomics |

|

1 |

Meaning |

Studies economic behavior

of individual decision-making units. (MP 2026) |

Studies economic behavior

of the entire economy as an aggregate whole. |

|

2 |

Alternative Name / Theory |

Known as Price Theory

(explains individual price determination). |

Known as Income and

Employment Theory (explains aggregate national metrics). |

|

3 |

Core Elements Included |

Individual unit, small variables,

and individual price determination. (MP 2024) |

National income, aggregate

output, employment levels, and inflation. |

|

4 |

Key Assumptions |

Assumes macro variables

(like total output) remain constant. |

Assumes micro variables

(like resource allocation among firms) remain constant. |

|

5 |

Limitations |

(1) Unrealistic full

employment assumption. (2) Paradoxical aggregates (saving is good for an

individual but hurts national demand). (MP 2023) (v.v. imp) |

(1) Ignores internal

individual inequalities. (2) Complex implementation

policies. |

|

Test 1.4 1.

Microeconomics includes the study of: (MP 2024) (a) Individual unit (b) Small variables (c) Individual price determination (d) All of the above 2.

In Microeconomics ____________ units are studied. (MP 2023) 3.

Distinguish between Microeconomics and Macroeconomics on the basis

of meaning, alternative theory name, core elements, and limitations. (MP

2023 / MP 2024)

|