Chapter 1: Accounting for Partnership – Basic Concepts

Chapter – 1.

Accounting

for Partnership – Basic Concepts

1.1

Nature and Essential Features of Partnership

1) Q.

Define Partnership according to Section 4 of the Indian Partnership Act, 1932.

Also, explain the terms ‘Partners’, ‘Firm’, and ‘Firm Name’. (MP 2024, NCERT)

Definition of Partnership: According to Section 4 of

the Indian Partnership Act, 1932: “Partnership is the relation between

persons who have agreed to share the profits of a business carried on by all or

any of them acting for all.”

- Partners: The persons who have

entered into a partnership with one another individually are called

‘Partners’.

- Firm: Collectively, all the

partners who run the business together are called a ‘Firm’.

- Firm Name: The specific name

under which the partnership business is conducted and managed is called

the ‘Firm Name’.

2) Q.

Explain the separate legal entity status of a partnership firm. Discuss it from

both an accounting and a legal viewpoint. (MP 2023, NCERT)

A

partnership firm has a unique status regarding its identity, which must be

understood through two distinct viewpoints:

1.

From an Accounting Viewpoint: (separate business entity) From

the accounting perspective All transactions, capital accounts, drawings, and

profits are recorded in the books of accounts purely from the firm’s

perspective.

2.

From a Legal Viewpoint: (not separate legal entity) under

the Indian Partnership Act, 1932, The firm and the partners are one and the

same in the eyes of the law. This implies that if the firm’s assets are

insufficient to pay off its debts, the private or personal assets of the

partners can be legally used to clear the firm’s liabilities.

3) Q3.

Explain the essential features or characteristics of a partnership firm. (MP

2025, MP 2023, NCERT)

To form a valid partnership, the following essential

features must be present:

- Two or More Persons: Minimum 2 persons &

maximum partners are 50.

- Agreement: A partnership is born

out of an agreement. This agreement can be either oral (spoken) or

written.

- Lawful Business: The partners must

carry out a legal or lawful business. Co-ownership of a property without a

regular business does not create a partnership.

- Profit Sharing: The main objective of

the agreement must be to share the profits of the business.

If an association is formed purely for charity work, it cannot be called a

partnership.

- Mutual Agency: The business must be

carried on by all the partners or by any one of them acting for all. This

means every partner is both a principal (can bind other

partners) and an agent (is bound by other partners).

- Restriction on Transfer

of Share: No partner can

transfer or sell their ownership share in the firm to an outsider or

family member without obtaining the unanimous (100%) consent of all other

existing partners.

- Unlimited Liability: The liability of all

partners is joint, several, and unlimited. If the business assets are not

enough to pay off the debts, the personal properties of the partners can

be used to pay the creditors.

- Only Individuals Can Be

Partners: Only natural human

persons who are legally competent to enter into a contract can become

partners. An artificial legal entity, an association of persons, or

another firm cannot become a partner. Minors and persons of unsound mind

are excluded from signing a regular partnership contract.

|

Quick Assessment 1.1

(a) Indian Partnership Act, 1930 (b)

Indian Partnership Act, 1932 (c) Company Act, 1956 (d)

Indian Partnership Act, 1931

|

1.2

Partnership Deed (Meaning, Importance, and Rules

in Absence)

4) Q:

What is a Partnership Deed? Explain its importance and list its key contents.

(MP 2024, NCERT)

Partnership Deed: The written document, which

contains the terms and conditions of the partnership agreed upon by all

partners, is called a Partnership Deed. It is also known as the Articles

of Partnership.

Key Contents of a

Partnership Deed

A

standard Partnership Deed generally contains the following clauses and details:

- Firm Details: Name and address of the firm, as well as its

main business activities.

- Partner Details: Names and addresses of all the individual

partners.

- Capital Contribution: The amount of capital to be contributed

by each partner, and whether the capital accounts will be fixed or

fluctuating.

- Profit-Sharing Ratio: The specific profit and loss sharing ratio among

partners.

- Interest on Capital and Drawings: The rate of interest

to be allowed on capitals and on drawings, if any.

- Partner Remuneration: The amount of salary, commission, or any

other remuneration payable to any partner.

- Interest on Loan: The rate of interest to be allowed on

loans advanced by a partner to the firm.

- Valuation of Goodwill: The methods for the

valuation of goodwill and assets in case of admission, retirement, or

death of a partner.

- Accounting Period: The accounting period of the firm and the

duration of the partnership.

- Settlement on Dissolution: The procedure for the

dissolution of the firm and the settlement of accounts.

5) Q:

Explain the practical importance of maintaining a written Partnership Deed. (MP

2023, NCERT)

Importance

of Partnership Deed

- Regulates Relations: It governs the rights, duties, and liabilities

of each individual partner as agreed upon mutually.

- Avoids Disputes: It helps in avoiding any misunderstandings,

conflicts, or disputes among partners because all terms and conditions are

pre-settled and documented.

- Legal Evidence: It serves as a reliable and valid proof in a

court of law in case any judicial dispute or litigation arises among the

partners in the future.

6) Q:

State the provisions or rules of the Indian Partnership Act, 1932 that apply to

the settlement of accounts in the absence of a Partnership Deed. (MP 2025, MP

2023, NCERT)

If the deed is silent on specific matters, the

provisions of the Indian Partnership Act, 1932 automatically apply to the

settlement of accounts. The core rules are as follows:

|

|

Matter |

Provision / Rule

Applicable act 1932 |

|

1 |

Sharing of Profits and

Losses |

Profits and losses are to

be shared equally among all the partners, irrespective of their

individual capital contributions. |

|

2 |

Interest on Capital |

No interest on capital shall be allowed or paid

to any partner. |

|

3 |

Interest on Drawings |

No interest on drawings shall be charged from any

partner on the amounts withdrawn by them. |

|

4 |

Interest on Partner’s Loan |

If a partner advances a

loan they are entitled to receive interest rate of 6% per annum. This

interest is a charge against profits, It must be paid even if the firm

suffers a loss. |

|

5 |

Remuneration to Partners |

No partner is entitled to

any salary, commission, or remuneration for taking part in the conduct or management of the

business. |

|

6 |

Admission of a partner |

only

with the consent of all the partners. |

Calculation of Commission

to Partners

1.

Net profit before

commission

2.

Net profit After

charging commission:

|

Quick Assessment: 1.2

(a) Indian Companies Act, 2013 (b) Indian Partnership

Act, 1932 (c) Indian Contract Act, 1872 (d) Banking

Regulation Act, 1949

|

1.3

Profit & Loss Appropriation Account

7) Q:

What is a Profit & Loss Appropriation Account? (MP 2024, NCERT)

A Profit & Loss

Appropriation Account is a special account prepared after the regular Profit

& Loss Account. Its primary purpose is to show how the net profit or net

loss of the firm is distributed or allocated among the partners according to

the provisions of the Partnership Deed or the rules of the Indian Partnership

Act, 1932.

8) Q:

Explain features/ characteristics of a Profit & Loss Appropriation Account.

(MP 2025, NCERT)

- Extension of P&L Account: It is prepared after

the finalization of the Profit & Loss Account and starts with the net

profit or net loss transferred from it.

- Nominal Account: It follows the rule of debiting all

appropriations that increase a partner’s claim (like interest on capital,

partner’s salary, or commission) and crediting items that decrease it

(like interest on drawings).

- Partnership Agreement Base: The entries passed in

this account are strictly guided by the clauses mentioned in the written

Partnership Deed or the legal rules applicable in its absence.

- Firm-Specific Preparation: It is prepared

specifically by partnership business entities to show allocation among

multiple owners, unlike sole proprietorship businesses where profits

belong to a single person.

9) Q:

Distinguish between Profit & Loss Account and Profit & Loss

Appropriation Account. (MP 2025, MP 2023, NCERT)

|

Basis |

Profit

& Loss Account |

Profit

& Loss Appropriation Account |

|

Stage

of Preparation |

Prepared

after the Trading Account is finalized. |

Prepared

after the Profit & Loss Account is finalized. |

|

Objective |

Determines

the net profit or net loss earned by the business during an accounting year. |

Distributes

and allocates the net profit or loss among the partners. |

|

Items

Handled |

Debited

with operating/non-operating business expenses and credited with business

incomes. |

Debited

with items like interest on capital, salaries/commissions to partners, and

credited with interest on drawings. |

|

Nature

of Items |

Contains

charges against profit. |

Contains

appropriations of profit. |

10)

|

Quick Assessment: 1.3 1.

Profit & Loss Appropriation Account is a: (MP 2024) (a) Real Account (b)

Personal Account (c) Nominal

Account (d) Valuation Account 2.

Interest on a partner’s loan is treated as a __________ and is

debited to the Profit & Loss Account. (MP 2025) 3.

Under what financial circumstance will a partnership firm prepare a

Profit & Loss Account but omit entries in the Profit & Loss

Appropriation Account? (NCERT)

|

|

Basis

of Distinction |

Charge

against Profit |

Appropriation

of Profit |

|

Meaning |

Expense

deducted from revenue to determine the true net profit or loss of the firm. |

Distribution

of the final net profit among the partners under different heads. |

|

Compulsion |

Mandatory

payment that must be allowed even if the firm suffers a heavy loss during the

year. |

Made only

when there is a net profit available. No entry is done if the firm is in a loss. |

|

Accounting

Place |

Debited

directly to the Profit & Loss Account. |

Debited to

the Profit & Loss Appropriation Account. |

|

Examples |

Rent paid

to a partner for business premises or interest allowed on a partner’s loan. |

Interest

on capital, salary or commission paid to a partner, or transfer to general

reserve. |

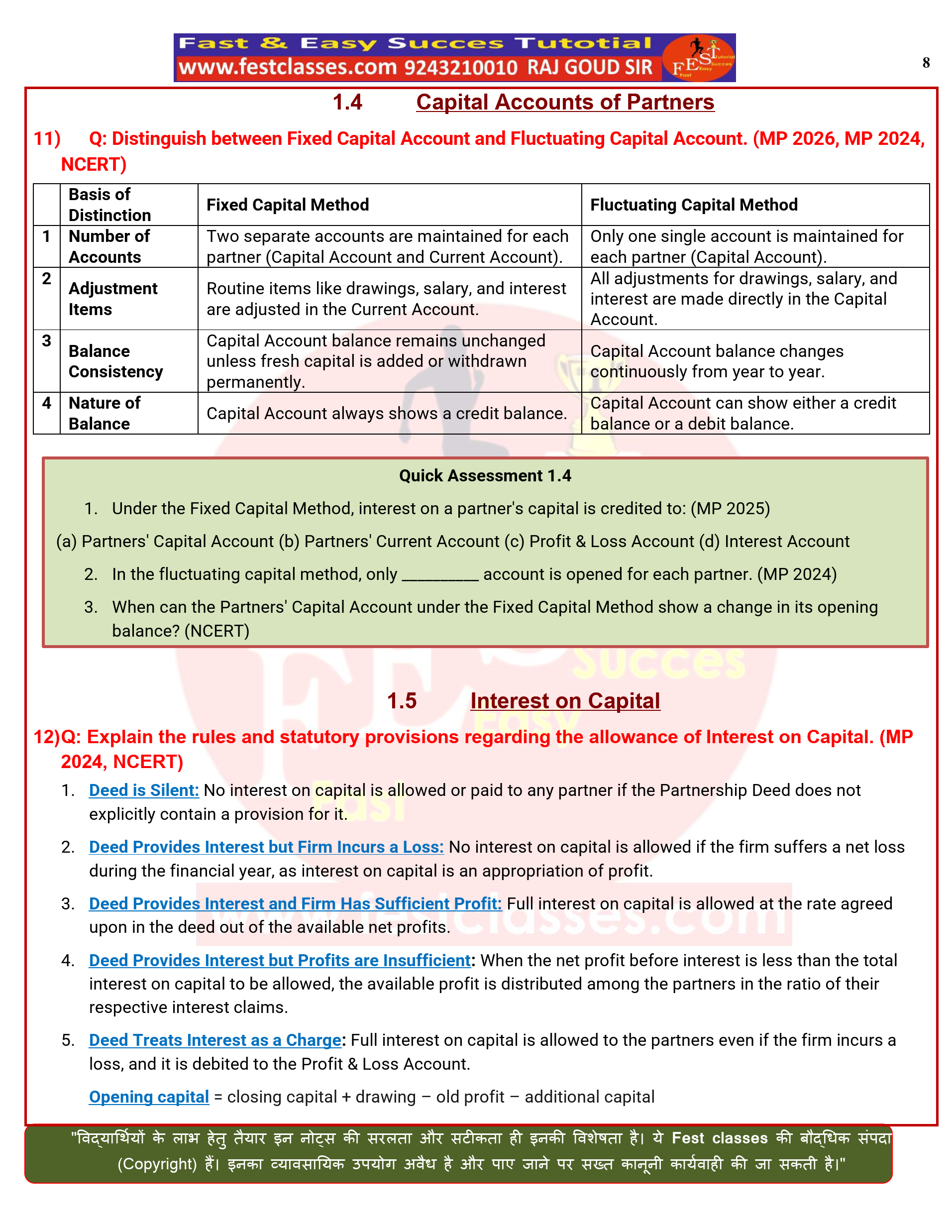

1.4

Capital Accounts of Partners

11)

Q: Distinguish between Fixed Capital Account and Fluctuating Capital

Account. (MP 2026, MP 2024, NCERT)

|

|

Basis

of Distinction |

Fixed

Capital Method |

Fluctuating

Capital Method |

|

1 |

Number

of Accounts |

Two

separate accounts are maintained for each partner (Capital Account and

Current Account). |

Only one

single account is maintained for each partner (Capital Account). |

|

2 |

Adjustment

Items |

Routine

items like drawings, salary, and interest are adjusted in the Current

Account. |

All

adjustments for drawings, salary, and interest are made directly in the

Capital Account. |

|

3 |

Balance

Consistency |

Capital

Account balance remains unchanged unless fresh capital is added or withdrawn

permanently. |

Capital

Account balance changes continuously from year to year. |

|

4 |

Nature

of Balance |

Capital

Account always shows a credit balance. |

Capital

Account can show either a credit balance or a debit balance. |

|

Quick Assessment 1.4

(a) Partners’ Capital Account (b) Partners’

Current Account (c) Profit & Loss Account (d) Interest Account

|

1.5

Interest on Capital

12) Q: Explain

the rules and statutory provisions regarding the allowance of Interest on

Capital. (MP 2024, NCERT)

- Deed is Silent: No interest on capital is allowed or paid to any

partner if the Partnership Deed does not explicitly contain a provision

for it.

- Deed Provides Interest but Firm Incurs a Loss: No interest on capital

is allowed if the firm suffers a net loss during the financial year, as

interest on capital is an appropriation of profit.

- Deed Provides Interest and Firm Has Sufficient

Profit:

Full interest on capital is allowed at the rate agreed upon in the deed

out of the available net profits.

- Deed Provides Interest but Profits are Insufficient: When the net profit

before interest is less than the total interest on capital to be allowed,

the available profit is distributed among the partners in the ratio of

their respective interest claims.

- Deed Treats Interest as a Charge: Full interest on

capital is allowed to the partners even if the firm incurs a loss, and it

is debited to the Profit & Loss Account.

Opening

capital =

closing capital + drawing – old profit – additional capital

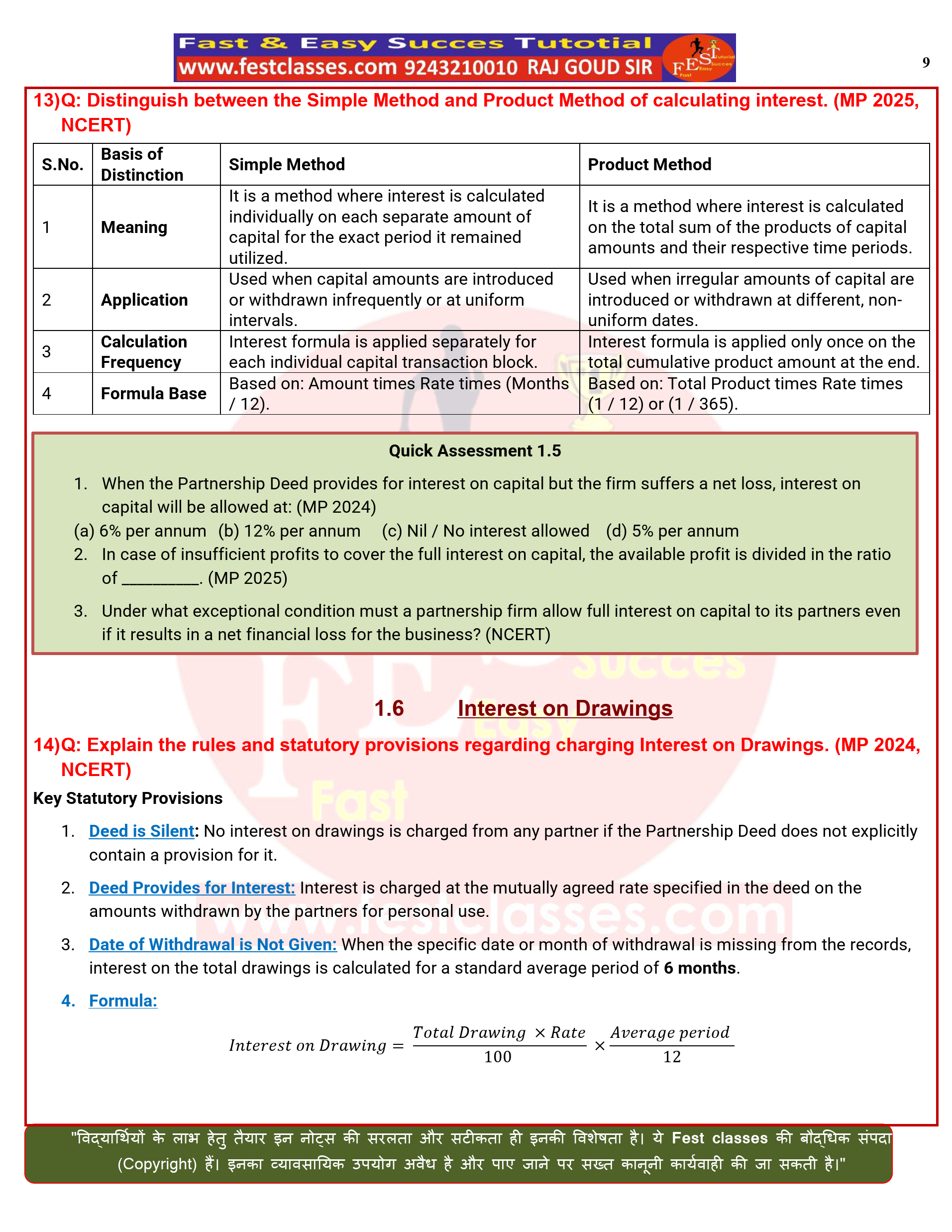

13)

|

Quick Assessment 1.5

(a) 6% per annum (b) 12% per annum (c) Nil / No interest allowed (d) 5% per annum

|

|

S.No. |

Basis of Distinction |

Simple Method |

Product Method |

|

1 |

Meaning |

It is a method where

interest is calculated individually on each separate amount of capital for

the exact period it remained utilized. |

It is a method where

interest is calculated on the total sum of the products of capital amounts

and their respective time periods. |

|

2 |

Application |

Used when capital amounts

are introduced or withdrawn infrequently or at uniform intervals. |

Used when irregular

amounts of capital are introduced or withdrawn at different, non-uniform

dates. |

|

3 |

Calculation Frequency |

Interest formula is

applied separately for each individual capital transaction block. |

Interest formula is

applied only once on the total cumulative product amount at the end. |

|

4 |

Formula Base |

Based on: Amount times Rate

times (Months / 12). |

Based on: Total Product

times Rate times (1 / 12) or (1 / 365). |

1.6

Interest on Drawings

14) Q: Explain

the rules and statutory provisions regarding charging Interest on Drawings. (MP

2024, NCERT)

Key

Statutory Provisions

- Deed is Silent: No interest on drawings is charged from any

partner if the Partnership Deed does not explicitly contain a provision

for it.

- Deed Provides for Interest: Interest is charged at

the mutually agreed rate specified in the deed on the amounts withdrawn by

the partners for personal use.

- Date of Withdrawal is Not Given: When the specific date

or month of withdrawal is missing from the records, interest on the total

drawings is calculated for a standard average period of 6 months.

4.

Formula:

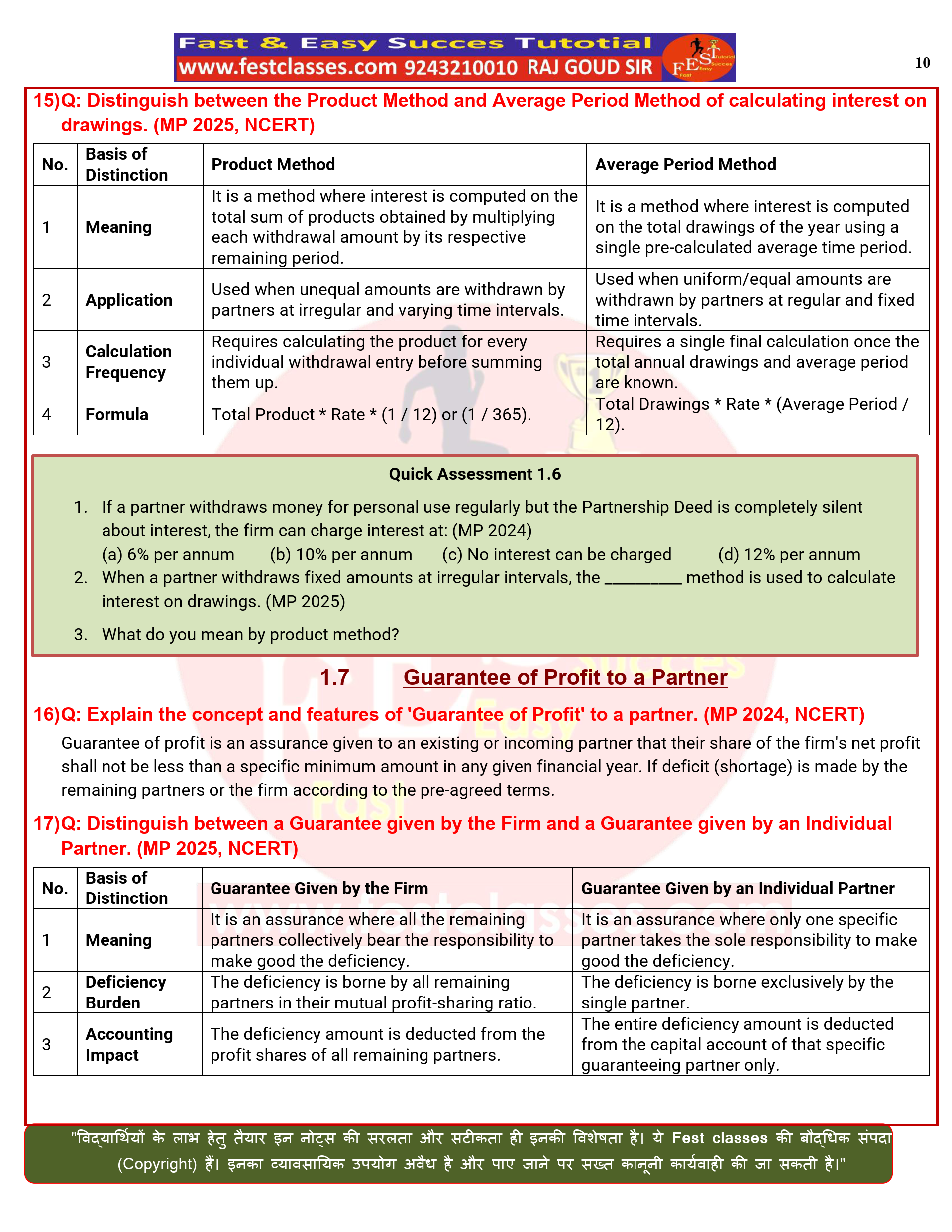

15)

|

Quick Assessment 1.6

(a) 6% per annum (b) 10% per annum (c) No interest can be charged (d) 12% per annum

|

|

No. |

Basis of Distinction |

Product Method |

Average Period Method |

|

1 |

Meaning |

It is a method where

interest is computed on the total sum of products obtained by multiplying

each withdrawal amount by its respective remaining period. |

It is a method where

interest is computed on the total drawings of the year using a single

pre-calculated average time period. |

|

2 |

Application |

Used when unequal amounts

are withdrawn by partners at irregular and varying time intervals. |

Used when uniform/equal

amounts are withdrawn by partners at regular and fixed time intervals. |

|

3 |

Calculation Frequency |

Requires calculating the

product for every individual withdrawal entry before summing them up. |

Requires a single final

calculation once the total annual drawings and average period are known. |

|

4 |

Formula |

Total Product * Rate * (1

/ 12) or (1 / 365). |

Total Drawings * Rate * (Average

Period / 12). |

1.7

Guarantee of Profit to a Partner

16) Q: Explain

the concept and features of ‘Guarantee of Profit’ to a partner. (MP 2024,

NCERT)

Guarantee of profit is an assurance given to an

existing or incoming partner that their share of the firm’s net profit shall

not be less than a specific minimum amount in any given financial year. If

deficit (shortage) is made by the remaining partners or the firm according to

the pre-agreed terms.

17) Q:

Distinguish between a Guarantee given by the Firm and a Guarantee given by an

Individual Partner. (MP 2025, NCERT)

|

No. |

Basis of Distinction |

Guarantee Given by the

Firm |

Guarantee Given by an

Individual Partner |

|

1 |

Meaning |

It is an assurance where

all the remaining partners collectively bear the responsibility to make good

the deficiency. |

It is an assurance where

only one specific partner takes the sole responsibility to make good the

deficiency. |

|

2 |

Deficiency Burden |

The deficiency is borne by

all remaining partners in their mutual profit-sharing ratio. |

The deficiency is borne

exclusively by the single partner. |

|

3 |

Accounting Impact |

The deficiency amount is

deducted from the profit shares of all remaining partners. |

The entire deficiency

amount is deducted from the capital account of that specific guaranteeing

partner only. |

|

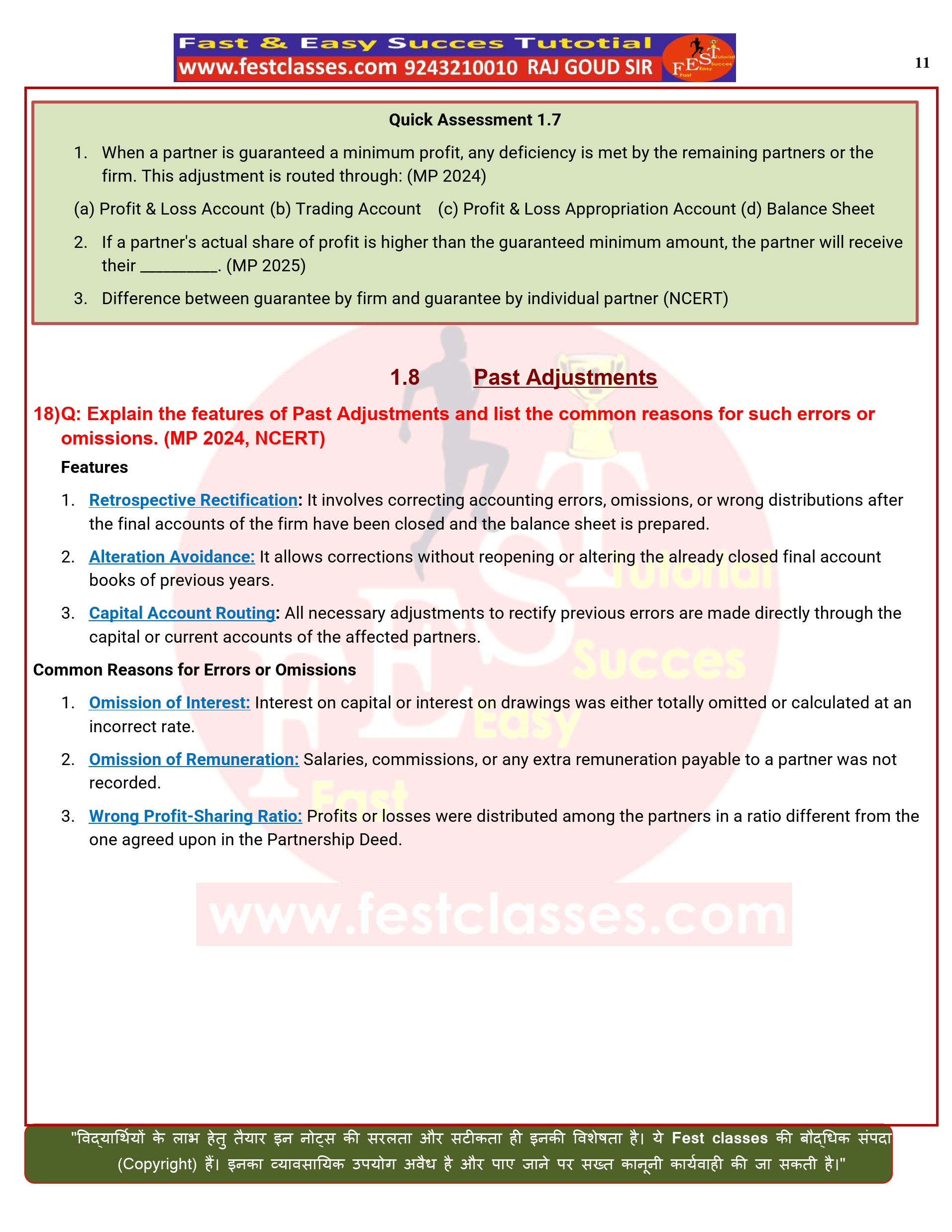

Quick Assessment 1.7

(a) Profit & Loss Account (b) Trading Account (c) Profit & Loss Appropriation Account (d) Balance Sheet

|

1.8

Past Adjustments

18) Q: Explain

the features of Past Adjustments and list the common reasons for such errors or

omissions. (MP 2024, NCERT)

Features

- Retrospective Rectification: It involves correcting

accounting errors, omissions, or wrong distributions after the final

accounts of the firm have been closed and the balance sheet is prepared.

- Alteration Avoidance: It allows corrections without reopening

or altering the already closed final account books of previous years.

- Capital Account Routing: All necessary

adjustments to rectify previous errors are made directly through the

capital or current accounts of the affected partners.

Common

Reasons for Errors or Omissions

- Omission of Interest: Interest on capital or interest on

drawings was either totally omitted or calculated at an incorrect rate.

- Omission of Remuneration: Salaries, commissions,

or any extra remuneration payable to a partner was not recorded.

- Wrong Profit-Sharing Ratio: Profits or losses were

distributed among the partners in a ratio different from the one agreed

upon in the Partnership Deed.

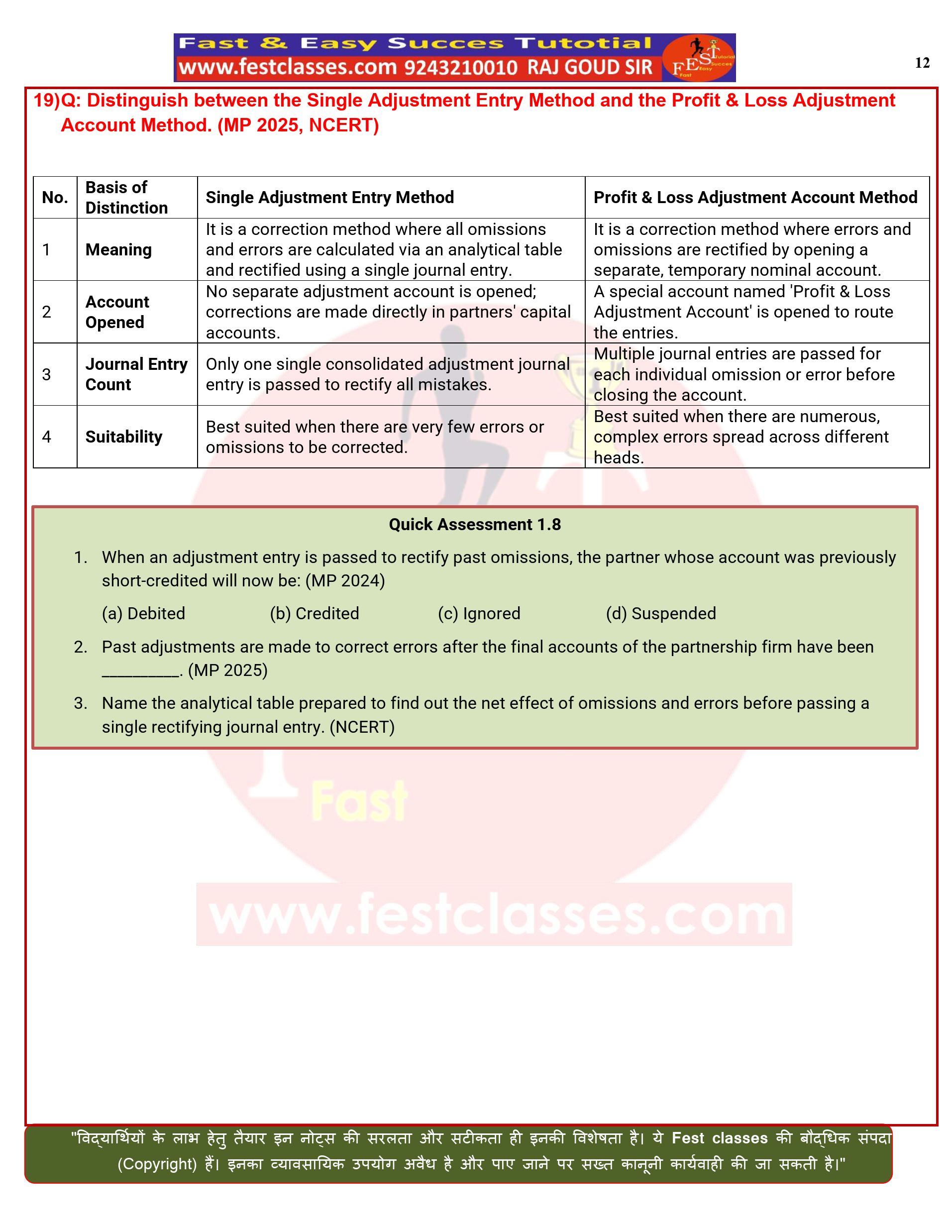

19) Q:

Distinguish between the Single Adjustment Entry Method and the Profit &

Loss Adjustment Account Method. (MP 2025, NCERT)

|

No. |

Basis of Distinction |

Single Adjustment Entry

Method |

Profit & Loss

Adjustment Account Method |

|

1 |

Meaning |

It is a correction method

where all omissions and errors are calculated via an analytical table and

rectified using a single journal entry. |

It is a correction method

where errors and omissions are rectified by opening a separate, temporary

nominal account. |

|

2 |

Account Opened |

No separate adjustment

account is opened; corrections are made directly in partners’ capital

accounts. |

A special account named

‘Profit & Loss Adjustment Account’ is opened to route the entries. |

|

3 |

Journal Entry Count |

Only one single

consolidated adjustment journal entry is passed to rectify all mistakes. |

Multiple journal entries

are passed for each individual omission or error before closing the account. |

|

4 |

Suitability |

Best suited when there are

very few errors or omissions to be corrected. |

Best suited when there are

numerous, complex errors spread across different heads. |

|

Quick Assessment 1.8

(a) Debited (b) Credited (c)

Ignored (d) Suspended

|